what is damage to your work perfotmed by subcontractor exclusion

Contractors: do yourself a favor and consult your insurance broker regarding your commercial full general liability (CGL) policy. Do this now, especially if you subcontract out piece of work.

Contractors: do yourself a favor and consult your insurance broker regarding your commercial full general liability (CGL) policy. Do this now, especially if you subcontract out piece of work.

CGL policies contain a "your work" exclusion . The CGL policy is written such that it excludes "' belongings impairment' to 'your piece of work' arising out of information technology or whatever part of it and included in the 'products-completed operations hazard.' " This exclusion volition be raised in the post-completion latent construction defect scenario. (In that location are other exclusions that will be raised to a defect discovered during construction.) Sure policies volition contain a subcontractor exception to this "your work" exclusion. You Desire this exception- no uncertainty about it so that this exclusion does not apply to work performed past your subcontractors. Without this subcontractor exception, truth be told, this "your work" exclusion is a total back-breaker to contractors. It volition give your insurer an immediate out for many latent defect property scenarios since excluded from coverage is belongings damage to your piece of work including work performed by your subcontractors.

In a recent opinion, Mid-Continent Casualty Co. v. JWN Construction, Inc., 2018 WL 783102 (S.D.Fla. 2018), an owner discovered water intrusion and damage at his belongings. He sued the general contractor and the general contractor's insurer filed a carve up action for declaratory relief claiming it had NO duty to defend or indemnify its insured—the full general contractor—in the underlying adjust. The courtroom agreed because the contractor did non have the subcontractor exception to the "your piece of work" exclusion.

If piece of work was performed by JWN [contractor] or on JWN's behalf-hither past a subcontractor-then the "your work" exclusion applies. Historically, insurers could exist liable under commercial general liabilities policies resembling the policy in the instant case for certain types of damages caused by subcontractors….Nonetheless, insurers exercise possess the correct to define their coverage as excluding damages arising out of a subcontractor's defective work by eliminating subcontractor's exceptions from the policy. An insurer is only liable for a subcontractor's defective work when the "your work" exclusion does not eliminate coverage for work performed past a subcontractor….In conclusion, the insurance policy in this instance excluded coverage for piece of work performed non only by JWN, but also by JWN's subcontractors.

JWN Construction, Inc., supra, at *iv.

This ruling meant that the general contractor's CGL insurer had no duty to defend or indemnify its insured—once again, the contractor—for the defects or resulting water impairment. A total killer illustrating the absolute importance of the subcontractor exception to the "your work" exclusion in your CGL policy.

Please contact David Adelstein at dadelstein@gmail.com or (954) 361-4720 if you have questions or would like more than data regarding this article. You can follow David Adelstein on Twitter @DavidAdelstein1.

I previously discussed the importance of the subcontractor exception to the "your work" exclusion in CGL policies (exclusion l) for contractors and subcontractors that subcontract out scopes of piece of work. Without this exception, the CGL policy provides minimal (and I hateful minimal) coverage for property damage associated with construction defects. If you are involved in construction, y'all categorically need to make certain there is a subcontractor exception to the "your work" exclusion in your CGL policy. The subcontractor exception to the "your work" exclusion is the linguistic communication bolded beneath that negates the application of the exclusion:

I previously discussed the importance of the subcontractor exception to the "your work" exclusion in CGL policies (exclusion l) for contractors and subcontractors that subcontract out scopes of piece of work. Without this exception, the CGL policy provides minimal (and I hateful minimal) coverage for property damage associated with construction defects. If you are involved in construction, y'all categorically need to make certain there is a subcontractor exception to the "your work" exclusion in your CGL policy. The subcontractor exception to the "your work" exclusion is the linguistic communication bolded beneath that negates the application of the exclusion:

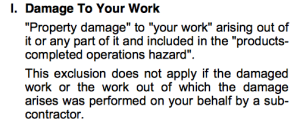

This insurance does not apply to:

50. Harm to Your Work

"Property damage" to "your piece of work" arising out of information technology or whatever part of it and included in the "products-completed operations chance".

This exclusion does not utilise if the damaged work or the piece of work out of which the harm arises was performed on your behalf by a subcontractor .

The Centre District in Motorcar-Owners Ins. Co. five. Elite Homes, Inc., 2016 WL 409577 (M.D.Fla. 2016) recently issued an opinion involving the application of the "your work" exclusion in a homebuilder's CGL policy that did non have the subcontractor exception (the language bolded higher up). Ouch!!!! Without this exception, the policy excluded from coverage "property harm to your piece of work arising out of it or any part of it and included in the products-completed operations hazard." Elite Homes, supra, at *2. But over again,at that place was no subcontractor exception that negated the application of this provision to work performed past a subcontractor.

What is the impact of not having the subcontractor exception to the "your work" exclusion? This case explains. The owners sued the homebuilder for water intrusion and harm from window defects. The complaint alleged that the leaky window(s) caused impairment to drywall, insulation, interior finishes, wood frame, and sheathing. The homebuilder's CGL insurer denied the homebuilder a defence and coverage based on the "your work" exclusion—the owner declared harm to the homebuilder's piece of work (the structure of the home) but nothing else. The Middle District concurred that the water harm alleged in the owner's complaint arose out of the homebuilder's piece of work and was harm to the homebuilder'south work (the abode). Hence, the "your work" exclusion barred coverage for the possessor's construction defect lawsuit against the homebuilder.

This opinion is painful considering information technology illustrates the non-value the CGL policy provided to the homebuilder for property harm associated with defective windows. This outcome was the event of a CGL policy that eliminated the subcontractor exception to the "your work" exclusion. If the policy had this subcontractor exception, then there would have been coverage for the water damage acquired by the defective windows and the homebuilder's CGL insurer would accept been obligated to defend the homebuilder in the possessor'south lawsuit. The homebuilder would have been able to say that information technology hired a glazer (subcontractor) that performed the window installation and the glazer'due south lacking window installation acquired impairment to other subcontractors' work.

Make sure to review your CGL policy. If you do not have the subcontractor exception to the "your work" exclusion, the effect in this example could probable be the result in your case dealing with property harm acquired past defective construction. Consult with your insurance banker considering this subcontractor exception to the "your piece of work" exclusion is a must in construction !

Please contact David Adelstein at dadelstein@gmail.com or (954) 361-4720 if yous have questions or would like more data regarding this commodity. You can follow David Adelstein on Twitter @DavidAdelstein1.

The recent Eleventh Circuit conclusion in J.B.D. Structure, Inc. v. Mid-Contintent Prey Co., 2014 WL 3377690 (11th Cir. 2014), demonstrates the unfortunate applicability of the "your work" exclusion in CGL policies when the subcontractor exception (meet epitome) to this exclusion was eliminated from the policy through an endorsement. This subcontractor exception to the "your piece of work" exclusion is important…I repeat, important…to the full general contractor and anyone performing construction work that subcontracts out their work. Realizing the subcontractor exception to the "your work" exclusion has been removed or eliminated through an endorsement volition create the dreadful "Oh No!" (or i its many wonderful euphemisms) moment! Just ask the contractor in J.B.D. Construction.

The recent Eleventh Circuit conclusion in J.B.D. Structure, Inc. v. Mid-Contintent Prey Co., 2014 WL 3377690 (11th Cir. 2014), demonstrates the unfortunate applicability of the "your work" exclusion in CGL policies when the subcontractor exception (meet epitome) to this exclusion was eliminated from the policy through an endorsement. This subcontractor exception to the "your piece of work" exclusion is important…I repeat, important…to the full general contractor and anyone performing construction work that subcontracts out their work. Realizing the subcontractor exception to the "your work" exclusion has been removed or eliminated through an endorsement volition create the dreadful "Oh No!" (or i its many wonderful euphemisms) moment! Just ask the contractor in J.B.D. Construction.

In this case, a general contractor was hired to construct a fitness center every bit an add-on to an existing building. The fitness center was going to be constructed with prefabricated components making up the shell, slab, and flooring. The general contractor engaged subcontractors to install the prefabricated components and subcontractors to install the required mechanical, electric, and plumbing.

Afterward construction, h2o damage was discovered in the fitness center acquired by leaks from the roof, windows, and doors. The water harm consisted of blistering stucco, rusting steel, and the peeling paint. The general contractor implemented repair measures to cease the water intrusion. The owner, nonetheless, refused to pay the general contractor its concluding payment. The full general contractor filed a lawsuit for this payment and the owner filed a counterclaim due to the leaks for breach of contract, negligence, and a violation of building code. The owner's counterclaim alleged that the general contractor's deficient work caused "damages to the interior of the property, other edifice components and materials, and other, consequential and resulting amercement" as well equally "damage to other property." J.B.D. Construction, supra, at *two.

At event was whether the general contractor'southward commercial general liability (CGL) carrier owed the insured-general contractor a duty to defend and duty to indemnify. In particular, the general contractor tendered the owner's counterclaim to its insurer for defense and indemnification. While the CGL insurer was conducting its investigation to determine if it would provide a defense, the full general contractor settled the counterclaim with the owner, paying the owner from its own funds. The general contractor so notified its insurer of the settlement and required reimbursement (indemnification) for the settlement corporeality in addition to legal/defense costs information technology incurred. Thereafter, the insurer tendered an amount information technology determined information technology owed for legal fees minus the policy'due south deductible, merely did not reimburse the general contractor for the settlement corporeality.

The trial court granted the insurer's motion for summary judgment in function finding that if any of the owner's claims were for costs to repair the defectively installed roof, windows, and doors, these costs were Non covered by the policy—they were excluded under the "your work" exclusion. The trial court farther stated that the insurer did NOT accept a duty to defend or indemnify the full general contractor in the counterclaim because there was nothing in the counterclaim that alleged damage to belongings other than to the fettle eye (the "your work").

The trial court granted the insurer's motion for summary judgment in function finding that if any of the owner's claims were for costs to repair the defectively installed roof, windows, and doors, these costs were Non covered by the policy—they were excluded under the "your work" exclusion. The trial court farther stated that the insurer did NOT accept a duty to defend or indemnify the full general contractor in the counterclaim because there was nothing in the counterclaim that alleged damage to belongings other than to the fettle eye (the "your work").

The "your work" exclusion in the policy excluded:

l. Damage to Your Work

"Property damage" to "your work" arising out of it or whatever part of it and included in the "products-completed operations hazard."

This exclusion did not include what is commonly known as the subcontractor exception to the "your work" exclusion that says this exclusion does not use if the damaged work or work out of which the harm arose was performed past a subcontractor. This is the Oh No! moment! Information technology turned out that the subcontractor exception was eliminated through an endorsement that completely inverse the application of the "your piece of work" exclusion.

The Eleventh Circuit made information technology clear that removing or replacing defectively installed work is non belongings damage covered past the CGL policy. Ok. That should be clear. But, what well-nigh resulting damage or harm that arose from the defective piece of work? With the subcontractor exception to the "your piece of work" exclusion, resulting damage should be covered if the defective piece of work was performed past a subcontractor; in other words, damage to some other subcontractor's work (e.grand., drywall, flooring) should exist covered if the impairment arose out of a split subcontractor'south defective work (e.g., roofer, glazer). The question, though, is whether this resulting harm is covered if the subcontractor exception was eliminated from the "your work" exclusion. Hence, if a roof leaks and causes impairment to other holding or work not performed by the roofing subcontractor, would this resulting damage be covered? The Eleventh Circuit held NO as any claims against the general contractor for damage to the fettle center ("your work") arising from the general contractor or its subcontractors' defective work are Not covered under the policy:

Originally, the MCC Policy [CGL policy] as well included a subcontractor exception to the "your work" exclusion, which stated that the "your piece of work" exclusion did "not apply if the damaged work or the piece of work out of which the damage arises was performed on your behalf past a subcontractor." As originally written, therefore, the MCC Policy covered claims for impairment to J.B.D.'s [full general contractor] "work" arising from the faulty structure of J.B.D.'s subcontractors. Withal, this exception was eliminated by Endorsement CG 22 94 101 01. Past eliminating the subcontractor's exception, the MCC Policy no longer covered whatever claims for damage to J.B.D.'s "work" arising from work performed by J.B.D.'due south subcontractors.

***

Therefore, the "your work" exclusion, absent the subcontractor's exception, bars coverage for damages to the completed fitness center or its components (J.B.D.'s "work") arising from J.B.D. or its subcontractor's defective construction.

J.B.D. Construction, supra, at *6-7.

At present, even though the Eleventh Circuit held that there was no CGL coverage (thus, no duty for the insurer to indemnify the general contractor), the insurer still had a duty to defend. How could this be? Because the duty to defend is broader than the duty to indemnify and is dictated by the allegations in the complaint. If a complaint potentially triggers coverage, the insurer has a duty to defend unless there is an exclusion that applies to bar coverage based strictly on the allegations in the complaint. Since the complaint alleged fizz language "damage to other property" caused by the full general contractor's actions, this arguably included damage to non-fitness center property that would be covered and not considered the general contractor's piece of work. Based on this, and even though the Eleventh Circuit held that the insurer did not have to reimburse the general contractor for the settlement amount paid the owner, information technology found that the insurer breached the duty to defend past not defending the general contractor with respect to the counterclaim. The insurer argued that it tendered defence costs to the general contractor based on the attorney's fees the general contractor incurred from the engagement of the tender to the insurer through the settlement with a deduct for the deductible. The Eleventh Excursion did not buy this argument stating that the general contractor accepted the coin making it clear that it was not in satisfaction of the general contractor's merits for additional payments/costs. For this reason, the Eleventh Circuit remanded the case back to the trial court to decide whether the general contractor is entitled to damages, including consequential damages, as a effect of the insurer's breach of its duty to defend the general contractor.

Practical Considerations

- For the general contractor (or subcontractors that engage sub-subcontractors) – Wait at your CGL policy. Does it have the subcontractor exception to the "your work" exclusion? If and so, is there an endorsement that eliminates this subcontractor exception. In this case, it was endorsement CG 22 94 101 01 (encounter image without subcontractor exception) that merely did not include the subcontractor exception language. Yous do NOT desire this endorsement as it strengthens the "your work" exclusion for many structure defect claims. Again, every bit a contractor that subcontracts piece of work, you lot exercise Not want an endorsement eliminating the subcontractor exception.

- For the party asserting the complaint and party receiving the complaint– Remember the duty of the insurer to defend its insured is broader than the duty to indemnify so include buzz language in the complaint that there is "harm to other belongings" other than the piece of work itself . It is always skillful to review the insurance policy of a party that you are suing to see whether there is an endorsement that eliminates the subcontractor exception to the "your work" exclusion. But, irrespective of whether yous accept the policy, including general buzz language could at least bring an insurer to the table and give an statement to the insured-accused to get its insurer to defend the allegations in the complaint. If the insurer refuses to defend, there may be a potential artery to explore that the insurer breached its duty to defend that may entitle the insured to certain, provable amercement.

Delight contact David Adelstein at dadelstein@gmail.com or (954) 361-4720 if yous have questions or would like more information regarding this article. You can follow David Adelstein on Twitter @DavidAdelstein1.

Source: https://www.floridaconstructionlegalupdates.com/tag/your-work-exclusion/

0 Response to "what is damage to your work perfotmed by subcontractor exclusion"

Post a Comment